Proforma Of A Reconciliation Statement 6d2d6p

This document was ed by and they confirmed that they have the permission to share it. If you are author or own the copyright of this book, please report to us by using this report form. Report l4457

Overview 6h3y3j

& View Proforma Of A Reconciliation Statement as PDF for free.

More details h6z72

- Words: 923

- Pages: 5

PROFORMA OF A RECONCILIATION STATEMENT

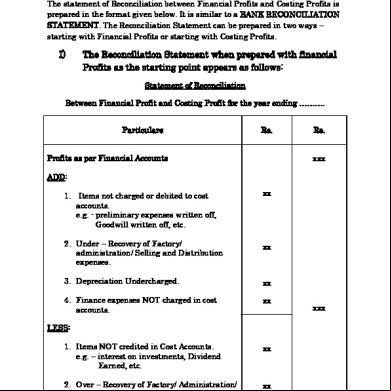

The statement of Reconciliation between Financial Profits and Costing Profits is prepared in the format given below. It is similar to a BANK RECONCILIATION STATEMENT. The Reconciliation Statement can be prepared in two ways – starting with Financial Profits or starting with Costing Profits.

I)

The Reconciliation Statement when prepared with financial Profits as the starting point appears as follows: Statement of Reconciliation

Between Financial Profit and Costing Profit for the year ending ………. Particulars

Rs.

Profits as per Financial s

Rs. xxx

ADD: 1. Items not charged or debited to cost s. e.g. - preliminary expenses written off, Goodwill written off, etc.

xx

2. Under – Recovery of Factory/ istration/ Selling and Distribution expenses.

xx

3. Depreciation Undercharged.

xx

4. Finance expenses NOT charged in cost s.

xx

xxx

LESS: 1. Items NOT credited in Cost s. e.g. – interest on investments, Dividend Earned, etc.

xx

2. Over – Recovery of Factory/ istration/ Selling and Distribution expenses.

xx

3. Depreciation overcharged

xx

Profits as per Cost s

xx

xxx xxx

II)

Reconciliation statement (starting with cost profits)

The basic rule for preparing the Reconciliation Statement i.e. “Do As The Other Has Done” is equally applicable in this case too. Thus, when we start with the costing profits, we have to do as the financial s have done. We have to start with the Cost Profits, and - exclude the items which we ignored by financial s. - Consider the items ed only in Financial s. - Adopt the amounts of stocks, depreciation, overheads, etc. adopted by financial s. - And finally adjust the costing profits accordingly. This process of „Doing What The Other Has Done‟ will finally reconcile the costing profits with the Financial Profits. Statement of Reconciliation Between Costing Profit and Financial Profits for the year ending …… Particulars

Rs.

Profits as per Cost s ADD: 1. Items NOT credited in Cost s. e.g. – interest on investments, dividend earned, etc. 2. Over recovery of Factory/ istration/ selling and Distribution expenses. 3. Depreciation. LESS: 1. Items NOT charged or Debited to Cost s. e.g. – Preliminary expenses written off, goodwill written off, etc. 2. Under Recovery of Factory/ istration/ selling and distribution expenses. 3. Depreciation undercharged. 4. Finance expenses NOT charged in cost s.

Rs. xxx

xxx xxx xxx

xxx

xxx

xxx xxx xxx xxx

Profit as per Financial s xxx

xxx

EXAMPLE OF RECONCILIATION STATEMENT

PROBLEM: A company named as „ARYA ENTERPRISES‟ furnishes its financial data or information in the form of Trading and Profit and Loss as follows : Particulars

Rs.

Purchase 37,815 Less : Closing stock 6,120 Wages [ Direct ] Works expenses Selling Expenses istration Expenses Depreciation Net Profit

31,695 15,750 18,195 10,650 8,010 1,650 30,450

TOTAL

1,16,400

Particulars

Rs.

Sales 75,000units @Rs.1.50each Profit on sale of Machinery

1,12,500 3,900

TOTAL

1,16,400

The profit as per Cost s was Rs. 29,655. Prepare Reconciliation Statement to reconcile Cost Profit with Financial Profits. Further information as per Cost s: (a) (b) (c)

Closing stock was taken at Rs.6,420 The works Expenses were taken at 100% of Direct Wages. Selling and istration Expenses were charged at 10% of sales and at Re.0.10 per unit respectively. (d) Depreciation was taken at Rs.1,200.

Solution:

Statement of Reconciliation Between Financial Profit and Costing Profit For the year ending …………..

Particulars

Rs.

Profit as per the FINANCIAL S ADD: 1.

Closing Stock Undervalued in Financial A/c (Rs.6,420 – Rs.6,120) 2. Depreciation Overcharged in Financial A/c (Rs.1,650 – Rs.1,200) 3.

Overheads Under recovered in Cost A/cs - Works Expenses (Rs.18,195 – Rs.15,750) - istration Expenses (Rs.8,010 – Rs. 7,500)

Rs. 30,450

300 450 2,445 510

3,705 34,155

LESS: 1. Income Credited in Financial A/cs only - Profit on Sale of Machinery 2. Overheads Over recovered in Cost A/cs - Selling expenses (Rs.11,250 – Rs.10650)

COSTING PROFIT

3,900

600 4,500

29,655

Conclusion Thus at the end of this very valuable project work we would like to conclude that the RECONCILIATION OF FINANCIAL AND COST STATEMENT is a necessary practice which must be undertaken by the management of each and every company which does not follows the integrated system of ing and whose financial statement’s profit does not tally with that of the profit of cost statements. The Reconciliation statement of Cost and Financial Statement is a statement which ensures accuracy of costing data furnished to the management on which many important decisions will be based. It also acts as a cross checks on both the sets of s and makes them reliable. In other words, the Reconciliation statement is a statement which determines the difference between the profits, if any shown by both the financial and cost s due to many reasons and tries to find out the reasons for such difference and further reconcile or amend it. This is how the concept of Reconciliation works. Though Reconciliation of financial and cost statement is very similar to a Bank Reconciliation statement but the significance or the value it has got is more than any statement since, it is the most important tool with the management with the help of which they can cross check the statements prepared both the departments i.e. Finance and cost and also assures reliability for quick decision making, saving future time and money, and a firm control of the management. Therefore it is quite essential and necessary for any company in this modern world to be equipped with this important tool as backup in their financial toolbox – RECONCILIATION OF FINANCIAL AND COST STATEMENT.

Thank you

The statement of Reconciliation between Financial Profits and Costing Profits is prepared in the format given below. It is similar to a BANK RECONCILIATION STATEMENT. The Reconciliation Statement can be prepared in two ways – starting with Financial Profits or starting with Costing Profits.

I)

The Reconciliation Statement when prepared with financial Profits as the starting point appears as follows: Statement of Reconciliation

Between Financial Profit and Costing Profit for the year ending ………. Particulars

Rs.

Profits as per Financial s

Rs. xxx

ADD: 1. Items not charged or debited to cost s. e.g. - preliminary expenses written off, Goodwill written off, etc.

xx

2. Under – Recovery of Factory/ istration/ Selling and Distribution expenses.

xx

3. Depreciation Undercharged.

xx

4. Finance expenses NOT charged in cost s.

xx

xxx

LESS: 1. Items NOT credited in Cost s. e.g. – interest on investments, Dividend Earned, etc.

xx

2. Over – Recovery of Factory/ istration/ Selling and Distribution expenses.

xx

3. Depreciation overcharged

xx

Profits as per Cost s

xx

xxx xxx

II)

Reconciliation statement (starting with cost profits)

The basic rule for preparing the Reconciliation Statement i.e. “Do As The Other Has Done” is equally applicable in this case too. Thus, when we start with the costing profits, we have to do as the financial s have done. We have to start with the Cost Profits, and - exclude the items which we ignored by financial s. - Consider the items ed only in Financial s. - Adopt the amounts of stocks, depreciation, overheads, etc. adopted by financial s. - And finally adjust the costing profits accordingly. This process of „Doing What The Other Has Done‟ will finally reconcile the costing profits with the Financial Profits. Statement of Reconciliation Between Costing Profit and Financial Profits for the year ending …… Particulars

Rs.

Profits as per Cost s ADD: 1. Items NOT credited in Cost s. e.g. – interest on investments, dividend earned, etc. 2. Over recovery of Factory/ istration/ selling and Distribution expenses. 3. Depreciation. LESS: 1. Items NOT charged or Debited to Cost s. e.g. – Preliminary expenses written off, goodwill written off, etc. 2. Under Recovery of Factory/ istration/ selling and distribution expenses. 3. Depreciation undercharged. 4. Finance expenses NOT charged in cost s.

Rs. xxx

xxx xxx xxx

xxx

xxx

xxx xxx xxx xxx

Profit as per Financial s xxx

xxx

EXAMPLE OF RECONCILIATION STATEMENT

PROBLEM: A company named as „ARYA ENTERPRISES‟ furnishes its financial data or information in the form of Trading and Profit and Loss as follows : Particulars

Rs.

Purchase 37,815 Less : Closing stock 6,120 Wages [ Direct ] Works expenses Selling Expenses istration Expenses Depreciation Net Profit

31,695 15,750 18,195 10,650 8,010 1,650 30,450

TOTAL

1,16,400

Particulars

Rs.

Sales 75,000units @Rs.1.50each Profit on sale of Machinery

1,12,500 3,900

TOTAL

1,16,400

The profit as per Cost s was Rs. 29,655. Prepare Reconciliation Statement to reconcile Cost Profit with Financial Profits. Further information as per Cost s: (a) (b) (c)

Closing stock was taken at Rs.6,420 The works Expenses were taken at 100% of Direct Wages. Selling and istration Expenses were charged at 10% of sales and at Re.0.10 per unit respectively. (d) Depreciation was taken at Rs.1,200.

Solution:

Statement of Reconciliation Between Financial Profit and Costing Profit For the year ending …………..

Particulars

Rs.

Profit as per the FINANCIAL S ADD: 1.

Closing Stock Undervalued in Financial A/c (Rs.6,420 – Rs.6,120) 2. Depreciation Overcharged in Financial A/c (Rs.1,650 – Rs.1,200) 3.

Overheads Under recovered in Cost A/cs - Works Expenses (Rs.18,195 – Rs.15,750) - istration Expenses (Rs.8,010 – Rs. 7,500)

Rs. 30,450

300 450 2,445 510

3,705 34,155

LESS: 1. Income Credited in Financial A/cs only - Profit on Sale of Machinery 2. Overheads Over recovered in Cost A/cs - Selling expenses (Rs.11,250 – Rs.10650)

COSTING PROFIT

3,900

600 4,500

29,655

Conclusion Thus at the end of this very valuable project work we would like to conclude that the RECONCILIATION OF FINANCIAL AND COST STATEMENT is a necessary practice which must be undertaken by the management of each and every company which does not follows the integrated system of ing and whose financial statement’s profit does not tally with that of the profit of cost statements. The Reconciliation statement of Cost and Financial Statement is a statement which ensures accuracy of costing data furnished to the management on which many important decisions will be based. It also acts as a cross checks on both the sets of s and makes them reliable. In other words, the Reconciliation statement is a statement which determines the difference between the profits, if any shown by both the financial and cost s due to many reasons and tries to find out the reasons for such difference and further reconcile or amend it. This is how the concept of Reconciliation works. Though Reconciliation of financial and cost statement is very similar to a Bank Reconciliation statement but the significance or the value it has got is more than any statement since, it is the most important tool with the management with the help of which they can cross check the statements prepared both the departments i.e. Finance and cost and also assures reliability for quick decision making, saving future time and money, and a firm control of the management. Therefore it is quite essential and necessary for any company in this modern world to be equipped with this important tool as backup in their financial toolbox – RECONCILIATION OF FINANCIAL AND COST STATEMENT.

Thank you

Related Documents 543cg

Proforma Of A Reconciliation Statement 6d2d6p

October 2019 84

Control Reconciliation Statement 133d51

November 2019 41

Bank Reconciliation Statement 35e2r

November 2021 0

Proforma Income Statement 614231

November 2019 62

Basic Instructions For A Bank Reconciliation Statement 2q405f

November 2019 57

Bank Reconciliation Statement-practice Problems 5y1uz

October 2019 111More Documents from "Atul Mumbarkar" 5u72w

Proforma Of A Reconciliation Statement 6d2d6p

October 2019 84

Anti Solution 1cf59

July 2021 0

Development Of Radio Journalism And Television Journalism 4go3m

December 2021 0

Mushroom Farming Bplan 3cr36

November 2019 141

Forgetting 4s6i2j

December 2021 0