Different Banking Channels For Customers 716s3f

This document was ed by and they confirmed that they have the permission to share it. If you are author or own the copyright of this book, please report to us by using this report form. Report l4457

Overview 6h3y3j

& View Different Banking Channels For Customers as PDF for free.

More details h6z72

- Words: 2,407

- Pages: 7

Executive Summery: DIFFERENT BANKING CHANNELS FOR CUSTOMERS Today’s customers often simultaneously used many banking channels. My study point out that a challenge for banks is how to connect with customers and provide financial services to them through the right channels, at the right time and in the right way. The challenges in Internet banking are related to business interaction between the bank and customer. It is crucial that the banking interaction is suited the customer's life situation. From this perspective it is important to give customers freedom to choose the most appropriate channel that best suits their preferences. In addition, the type of business affects customers’ choice of channel. Customers’ channel preferences vary between countries because of cultural differences, use-habits and legislation. The business interaction between the bank and the customer takes place through different channels . The interaction can be described as a continuum, which is described in Figure 1.

Figure 1. Different banking channels Figure 1 shows the different banking channels presented as a continuum where left side channels are limited by time and place and channels on the right side are more free from these constraints. The physical interaction between the bank and customer takes place in branch offices, which are limited in both time and location. By contrast Internet banking and mobile banking are the most flexible banking channels that are more free from constraints such as time and place. It has been proposed that a branch office is the primary channel for

purchasing many financial products because it offers the customer a secure physical location for the transaction of complex financial business with real people . The electronic banking, which provides many benefits, challenges, and opportunities for the whole banking sector. From the customer's point of view, Internet banking offers new value to customer because it makes available a full range of services that are not offered in branch offices . Modern Internet technology makes it possible to create customized banking services for every individual customer .Customers' value features in Internet banking such as convenience, increased choice of access to the bank, improved control over their banking activities and finances, ease of use, speed and security. From the banks perspective the main benefits of electronic banking are cost savings, reaching new segments of the population, efficiency, cross selling, third-party integration, and customer satisfaction.The success of banks operating via the Internet depends on their ability to attract and keep customers. Banks implement Internet banking services in an attempt to create powerful barriers to customers exiting. In general, it has been reported that Internet banking saves time and money, provides convenience and accessibility, and has a positive impact on customer satisfaction. Despite of these benefits Internet banking includes many challenges. The challenge of Internet banking is how to satisfy new online customer segments. The key factor in this competition for online customers is the quality of customer service, which includes usable interfaces of Internet banking. From this perspective the usability of Internet banking becomes an essential factor in the competition for online customers. INTRODUCTION In the recent years there has been explosion of Internet-based electronic banking applications .The emergence of new forms of technology has created highly competitive market conditions for bank providers. However, the changed market conditions demand for banks to better understanding of consumers' needs. The success in Internet banking will be achieved with tailored financial products and services that fulfill customer' wants, preferences and quality expectations.The customer satisfaction is a key to success in Internet banking and banks will use different media to customize products and services to fit customers' specific needs in the future. The consumer perceptions of transaction security, transaction accuracy, friendliness, and network speed are the critical factors for success in Internet banking. From this perspective, Internet banking includes many challenges for human computer interaction . There are at least two major challenges in Internet banking. The first challenge is related to the problem how to increase the number of services of Internet banking and simultaneously guarantee the quality of service for individual customers. The second challenge is related to the problem how to understand customer's needs, translate them into targeted content and present them in a personalized way in usable interface. DEFINITION OF ELECTRONIC BANKING The concept of electronic banking has been defined in many ways.It can be defined as electronic banking is a construct that consists of several distribution channels.It can also be defined as the delivery of banks' information and services by banks to customers via different delivery platforms that can be used with different terminal devices such as a

personal computer and a mobile phone with browser or desktop software, telephone or digital television. The different forms of electronic banking are summarized in Table 1.

Table 1. Different forms of banking in electronic banking (Daniel 1999) Form of Description banking PC banking The customer installs banking software on his or her personal computer. The customer has access to his or her with that specific software. Internet banking Customer can access his or her bank via the Internet using a PC or mobile phone and web-browser. TV-based The use of satellite or cable to deliver information to the TV banking screens of customers. Telephone-based Customers can access their bank and via SMS and as well as banking by ordinary phone using services of interactive voice responses (IVR).

Table 1. Different forms of banking in electronic banking. PC banking : The customer installs banking software on his or her personal computer. The customer has access to his or her with that specific software. Internet banking :Customer can access his or her bank via the Internet using a PC or mobile phone and web-browser. TV-based banking : The use of satellite or cable to deliver information to the TV screens of customers. Telephone based banking: Customers can access their bank and via SMS and as well as by ordinary phone using services of interactive voice responses (IVR).

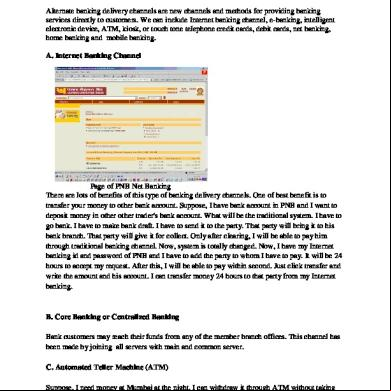

THE CONCEPT OF NET BANKING:

The internet revolution is changing the way we communicate and interact with the world around us. The medium of the net has opened up new vistas in commerce and banking and monetary transactions are done at the speed of light. E-commerce is the mantra of the

young, urban, upwardly mobile professional, who makes things happen at the click of a mouse. Nowadays, it's common to transact and do business on the net by using one's credit card. Ever wondered what happens when you punch in your credit card number on an internet website? Your credit card number travels to the site where somebody at the back-end receives the number, then punches it into an EDC terminal for approval from VISA and MasterCard. Because of the manual intervention, there is a risk of fraud, as the credit card number could be misused. Anybody who has access to your credit card number could order goods on any other site and you end up paying for it. Furthermore, the manual procedure makes the system slow in of the response time authorisation. HDFC bank launches India's first secure, online, real-time Internet Payment Gateway The concept of Virtual Banking or Internet banking was introduced in 1994. Now, HDFC Bank, for the first time in India, has made the e-shopping experience secure, on-line and real time with the launch of its payment gateway in May 2000. This will allow any Visa/Master Credit Card holder anywhere in the world to make payments for global services over the Internet. If you enter your credit card number on this gateway, not only does the credit card number travel in a secure mode to the site but also all the way to Visa and back to the site instantly, automatically, without the credit card number being visible to the shopping site or anybody else. HDFC has launched Depository Services on the Net, by which retail banking customers having a depository with them can now view their s through Net Banking. To avail this facility the customer will have to submit a form for getting his s ed to his customer ID. This service will be extended for all the s where the Net Banking customer is the first / sole holder in the Depository. The facilities that the investor can avail of through the net for depository services would include the following : • Holdings as on the close of the last business day. • Transactions for the last seven days. • Demat status of the shares submitted for demat in the last one month. • holders profile. • ISIN search to know the ISIN for a particular company. • CC Calendar to know the various settlement details on various exchanges. Netbanking customers can transfer funds from any of their s to any Third Party anywhere in the Bank. Transfers will be effected on an ONLINE and REALTIME basis. No more hassles of issuing outstation cheques / demand drafts, etc., to other holders of the Bank. HDFC Bank's BillPay facility allows you to pay your utility & cellular phone bills on the net from anywhere in the world, anytime. to the HDFC Bank website, select the bill payment option & the company for which you have to pay the bill. Enter in the bill amount you have to pay & confirm. Your will be automatically debited & payment made to the respective billing company the next working day. Net Banking has three basic features. They are as follows: • The banks offer only relevant informations about their products and services to the mass.

• Few banks provide interaction facility between the banks and its customers. • Banks are coming up with arrangements of utility payments, like telephone bills, electricity bills, etc. The current statistics show that hardly 10 per cent of Indian customers uses the internet for banking. Among all the facilities provided, the maximum of them uses only for checking balance or requesting for a cheque book. Very few customers uses the advance interactive services provided by the banks. According to HDFC and ICICI Bank, 17 per cent of ICICI customers use the Internet for banking and 10 per cent of HDFC customers prefer it.

Advantages of Net Banking • It removes the traditional geographical barriers as it could reach out to customers of different countries/legal jurisdiction. This has raised the question of jurisdiction of law/supervisory system to which such transactions should be subjected. • It has added a new dimension to different kinds of risks traditionally associated with banking, heightening some of them and throwing new risk control challenges. • Security of banking transactions, validity of electronic contract, customers' privacy, etc., which have all along been concerns of both bankers and supervisors have assumed different dimensions given that Internet is a public domain, not subject to control by any single authority or group of s. • It poses a strategic risk of loss of business to those banks who do not respond in time to this new technology, being the efficient and cost effective delivery.

HDFC Bank offers a new concept called Mobile Banking in association with Orange in Mumbai and Essar and AirTel in Delhi. A revolutionary new service, it enables you to access your HDFC Bank from your cellular phone. This service works on the SMS message (Text Message) function available on the mobile phone and is ed by their NetBanking infrastructure. You can conduct the following transactions using your mobile phone: Balance Enquiry

Last 3

transactions Statement Request Cheque Book RequestStop Cheque Request Set Operative FD Inquiry Cheque Status Bill Pay All transactions, barring the balance enquiry, are conducted on your operative , which is the you select. The balance enquiry transaction operates on all s linked to your customer ID. Customers in Mumbai are offered Mobile Commerce for the first time in India. If you are a resident of Mumbai, you can access your HDFC Bank and conduct financial transactions on your mobile phone screen. To use Mobile Commerce, open a Savings and for the Mobile Commerce and BillPay services. This facility offers to pay your electricity and mobile phone bills, enquire about pending bills of companies that you have ed under the BillPay facility, check the balance in the fixed deposits linked to your customer ID, etc.

Avail of the following services via PhoneBanking: 1)Check your balance - Get up-to-the-second details of your Savings or Current s and your Fixed Deposits. You can also get the details of the last 5 transactions on your , or have a mini statement of last 9 transactions faxed across to you. 2)Enquire on the cheque status - You can use PhoneBanking to check on the status of cheques issued or deposited from anywhere in India. 3)Order a Cheque Book / Statement - Just call PhoneBanking and get your Cheque Book or latest Statement delivered at your doorstep. 4)Stop Payment - Stop payment of a single cheque or a series of cheques, 24 hours a day. 5)Loan Related queries - Get details of the outstanding loan amount, enquire about your loan , request for an interest certificate and repayment schedule, etc. Just call PhoneBanking in your city and dial to PhoneBanker 6)Open a Fixed deposit or Enquire on your Fixed deposits - Talk to PhoneBanker to easily open a Fixed Deposit over the phone, by simply authorising a transfer of funds from your Savings .

7)Transfer Funds between s,You can also transfer money from one of your s to another. Both s must be linked to your Customer ID. You can transfer amounts upto Rs 1 Lac in a single day. 8)Pay your bills - Pay your cellular, telephone, electricity and HDFC Bank Credit Card bills through PhoneBanking using BillPay, a comprehensive bill payments solution. 9)Report loss of your ATM / Debit Card / ForexPlus Card - If your ATM / Debit / ForexPlus Card is lost, call any PhoneBanking number to deactivate your card(s). 10)Learn about all other products - Get details on HDFC Bank products & services by talking to our Phone Banker. 11)Enquire about latest Interest / Exchange rates - Get latest Interest rates on Deposits and Foreign Exchange rates by talking to our Phone Banker. 12) Request a Demand Draft / Manager's Cheque - Call PhoneBanking and get a Demand Draft / Manager's Cheque delivered to your doorstep.

Figure 1. Different banking channels Figure 1 shows the different banking channels presented as a continuum where left side channels are limited by time and place and channels on the right side are more free from these constraints. The physical interaction between the bank and customer takes place in branch offices, which are limited in both time and location. By contrast Internet banking and mobile banking are the most flexible banking channels that are more free from constraints such as time and place. It has been proposed that a branch office is the primary channel for

purchasing many financial products because it offers the customer a secure physical location for the transaction of complex financial business with real people . The electronic banking, which provides many benefits, challenges, and opportunities for the whole banking sector. From the customer's point of view, Internet banking offers new value to customer because it makes available a full range of services that are not offered in branch offices . Modern Internet technology makes it possible to create customized banking services for every individual customer .Customers' value features in Internet banking such as convenience, increased choice of access to the bank, improved control over their banking activities and finances, ease of use, speed and security. From the banks perspective the main benefits of electronic banking are cost savings, reaching new segments of the population, efficiency, cross selling, third-party integration, and customer satisfaction.The success of banks operating via the Internet depends on their ability to attract and keep customers. Banks implement Internet banking services in an attempt to create powerful barriers to customers exiting. In general, it has been reported that Internet banking saves time and money, provides convenience and accessibility, and has a positive impact on customer satisfaction. Despite of these benefits Internet banking includes many challenges. The challenge of Internet banking is how to satisfy new online customer segments. The key factor in this competition for online customers is the quality of customer service, which includes usable interfaces of Internet banking. From this perspective the usability of Internet banking becomes an essential factor in the competition for online customers. INTRODUCTION In the recent years there has been explosion of Internet-based electronic banking applications .The emergence of new forms of technology has created highly competitive market conditions for bank providers. However, the changed market conditions demand for banks to better understanding of consumers' needs. The success in Internet banking will be achieved with tailored financial products and services that fulfill customer' wants, preferences and quality expectations.The customer satisfaction is a key to success in Internet banking and banks will use different media to customize products and services to fit customers' specific needs in the future. The consumer perceptions of transaction security, transaction accuracy, friendliness, and network speed are the critical factors for success in Internet banking. From this perspective, Internet banking includes many challenges for human computer interaction . There are at least two major challenges in Internet banking. The first challenge is related to the problem how to increase the number of services of Internet banking and simultaneously guarantee the quality of service for individual customers. The second challenge is related to the problem how to understand customer's needs, translate them into targeted content and present them in a personalized way in usable interface. DEFINITION OF ELECTRONIC BANKING The concept of electronic banking has been defined in many ways.It can be defined as electronic banking is a construct that consists of several distribution channels.It can also be defined as the delivery of banks' information and services by banks to customers via different delivery platforms that can be used with different terminal devices such as a

personal computer and a mobile phone with browser or desktop software, telephone or digital television. The different forms of electronic banking are summarized in Table 1.

Table 1. Different forms of banking in electronic banking (Daniel 1999) Form of Description banking PC banking The customer installs banking software on his or her personal computer. The customer has access to his or her with that specific software. Internet banking Customer can access his or her bank via the Internet using a PC or mobile phone and web-browser. TV-based The use of satellite or cable to deliver information to the TV banking screens of customers. Telephone-based Customers can access their bank and via SMS and as well as banking by ordinary phone using services of interactive voice responses (IVR).

Table 1. Different forms of banking in electronic banking. PC banking : The customer installs banking software on his or her personal computer. The customer has access to his or her with that specific software. Internet banking :Customer can access his or her bank via the Internet using a PC or mobile phone and web-browser. TV-based banking : The use of satellite or cable to deliver information to the TV screens of customers. Telephone based banking: Customers can access their bank and via SMS and as well as by ordinary phone using services of interactive voice responses (IVR).

THE CONCEPT OF NET BANKING:

The internet revolution is changing the way we communicate and interact with the world around us. The medium of the net has opened up new vistas in commerce and banking and monetary transactions are done at the speed of light. E-commerce is the mantra of the

young, urban, upwardly mobile professional, who makes things happen at the click of a mouse. Nowadays, it's common to transact and do business on the net by using one's credit card. Ever wondered what happens when you punch in your credit card number on an internet website? Your credit card number travels to the site where somebody at the back-end receives the number, then punches it into an EDC terminal for approval from VISA and MasterCard. Because of the manual intervention, there is a risk of fraud, as the credit card number could be misused. Anybody who has access to your credit card number could order goods on any other site and you end up paying for it. Furthermore, the manual procedure makes the system slow in of the response time authorisation. HDFC bank launches India's first secure, online, real-time Internet Payment Gateway The concept of Virtual Banking or Internet banking was introduced in 1994. Now, HDFC Bank, for the first time in India, has made the e-shopping experience secure, on-line and real time with the launch of its payment gateway in May 2000. This will allow any Visa/Master Credit Card holder anywhere in the world to make payments for global services over the Internet. If you enter your credit card number on this gateway, not only does the credit card number travel in a secure mode to the site but also all the way to Visa and back to the site instantly, automatically, without the credit card number being visible to the shopping site or anybody else. HDFC has launched Depository Services on the Net, by which retail banking customers having a depository with them can now view their s through Net Banking. To avail this facility the customer will have to submit a form for getting his s ed to his customer ID. This service will be extended for all the s where the Net Banking customer is the first / sole holder in the Depository. The facilities that the investor can avail of through the net for depository services would include the following : • Holdings as on the close of the last business day. • Transactions for the last seven days. • Demat status of the shares submitted for demat in the last one month. • holders profile. • ISIN search to know the ISIN for a particular company. • CC Calendar to know the various settlement details on various exchanges. Netbanking customers can transfer funds from any of their s to any Third Party anywhere in the Bank. Transfers will be effected on an ONLINE and REALTIME basis. No more hassles of issuing outstation cheques / demand drafts, etc., to other holders of the Bank. HDFC Bank's BillPay facility allows you to pay your utility & cellular phone bills on the net from anywhere in the world, anytime. to the HDFC Bank website, select the bill payment option & the company for which you have to pay the bill. Enter in the bill amount you have to pay & confirm. Your will be automatically debited & payment made to the respective billing company the next working day. Net Banking has three basic features. They are as follows: • The banks offer only relevant informations about their products and services to the mass.

• Few banks provide interaction facility between the banks and its customers. • Banks are coming up with arrangements of utility payments, like telephone bills, electricity bills, etc. The current statistics show that hardly 10 per cent of Indian customers uses the internet for banking. Among all the facilities provided, the maximum of them uses only for checking balance or requesting for a cheque book. Very few customers uses the advance interactive services provided by the banks. According to HDFC and ICICI Bank, 17 per cent of ICICI customers use the Internet for banking and 10 per cent of HDFC customers prefer it.

Advantages of Net Banking • It removes the traditional geographical barriers as it could reach out to customers of different countries/legal jurisdiction. This has raised the question of jurisdiction of law/supervisory system to which such transactions should be subjected. • It has added a new dimension to different kinds of risks traditionally associated with banking, heightening some of them and throwing new risk control challenges. • Security of banking transactions, validity of electronic contract, customers' privacy, etc., which have all along been concerns of both bankers and supervisors have assumed different dimensions given that Internet is a public domain, not subject to control by any single authority or group of s. • It poses a strategic risk of loss of business to those banks who do not respond in time to this new technology, being the efficient and cost effective delivery.

HDFC Bank offers a new concept called Mobile Banking in association with Orange in Mumbai and Essar and AirTel in Delhi. A revolutionary new service, it enables you to access your HDFC Bank from your cellular phone. This service works on the SMS message (Text Message) function available on the mobile phone and is ed by their NetBanking infrastructure. You can conduct the following transactions using your mobile phone: Balance Enquiry

Last 3

transactions Statement Request Cheque Book RequestStop Cheque Request Set Operative FD Inquiry Cheque Status Bill Pay All transactions, barring the balance enquiry, are conducted on your operative , which is the you select. The balance enquiry transaction operates on all s linked to your customer ID. Customers in Mumbai are offered Mobile Commerce for the first time in India. If you are a resident of Mumbai, you can access your HDFC Bank and conduct financial transactions on your mobile phone screen. To use Mobile Commerce, open a Savings and for the Mobile Commerce and BillPay services. This facility offers to pay your electricity and mobile phone bills, enquire about pending bills of companies that you have ed under the BillPay facility, check the balance in the fixed deposits linked to your customer ID, etc.

Avail of the following services via PhoneBanking: 1)Check your balance - Get up-to-the-second details of your Savings or Current s and your Fixed Deposits. You can also get the details of the last 5 transactions on your , or have a mini statement of last 9 transactions faxed across to you. 2)Enquire on the cheque status - You can use PhoneBanking to check on the status of cheques issued or deposited from anywhere in India. 3)Order a Cheque Book / Statement - Just call PhoneBanking and get your Cheque Book or latest Statement delivered at your doorstep. 4)Stop Payment - Stop payment of a single cheque or a series of cheques, 24 hours a day. 5)Loan Related queries - Get details of the outstanding loan amount, enquire about your loan , request for an interest certificate and repayment schedule, etc. Just call PhoneBanking in your city and dial to PhoneBanker 6)Open a Fixed deposit or Enquire on your Fixed deposits - Talk to PhoneBanker to easily open a Fixed Deposit over the phone, by simply authorising a transfer of funds from your Savings .

7)Transfer Funds between s,You can also transfer money from one of your s to another. Both s must be linked to your Customer ID. You can transfer amounts upto Rs 1 Lac in a single day. 8)Pay your bills - Pay your cellular, telephone, electricity and HDFC Bank Credit Card bills through PhoneBanking using BillPay, a comprehensive bill payments solution. 9)Report loss of your ATM / Debit Card / ForexPlus Card - If your ATM / Debit / ForexPlus Card is lost, call any PhoneBanking number to deactivate your card(s). 10)Learn about all other products - Get details on HDFC Bank products & services by talking to our Phone Banker. 11)Enquire about latest Interest / Exchange rates - Get latest Interest rates on Deposits and Foreign Exchange rates by talking to our Phone Banker. 12) Request a Demand Draft / Manager's Cheque - Call PhoneBanking and get a Demand Draft / Manager's Cheque delivered to your doorstep.

Related Documents 543cg

Different Banking Channels For Customers 716s3f

January 2022 0

Customers m3g42

April 2020 26

Types Of Banking And Types Of Banking Customers 1261j

October 2019 37

Channels 3b2w6r

December 2019 70

Channels 3b2w6r

July 2022 0