Company Law Notes (uk) 64x5d

This document was ed by and they confirmed that they have the permission to share it. If you are author or own the copyright of this book, please report to us by using this report form. Report l4457

Overview 6h3y3j

& View Company Law Notes (uk) as PDF for free.

More details h6z72

- Words: 67,126

- Pages: 140

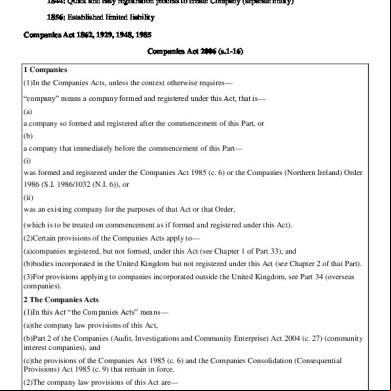

Lectures 1 & 2 Legislation: t Stock Companies Act 1844 and 1856 1844: Quick and easy registration process to create Company (separate entity) 1856: Established limited liability Companies Act 1862, 1929, 1948, 1985 Companies Act 2006 (s.1-16) 1 Companies (1)In the Companies Acts, unless the context otherwise requires— “company” means a company formed and ed under this Act, that is— (a) a company so formed and ed after the commencement of this Part, or (b) a company that immediately before the commencement of this Part— (i) was formed and ed under the Companies Act 1985 (c. 6) or the Companies (Northern Ireland) Order 1986 (S.I. 1986/1032 (N.I. 6)), or (ii) was an existing company for the purposes of that Act or that Order, (which is to be treated on commencement as if formed and ed under this Act). (2)Certain provisions of the Companies Acts apply to— (a)companies ed, but not formed, under this Act (see Chapter 1 of Part 33), and (b)bodies incorporated in the United Kingdom but not ed under this Act (see Chapter 2 of that Part). (3)For provisions applying to companies incorporated outside the United Kingdom, see Part 34 (overseas companies). 2 The Companies Acts (1)In this Act “the Companies Acts” means— (a)the company law provisions of this Act, (b)Part 2 of the Companies (Audit, Investigations and Community Enterprise) Act 2004 (c. 27) (community interest companies), and (c)the provisions of the Companies Act 1985 (c. 6) and the Companies Consolidation (Consequential Provisions) Act 1985 (c. 9) that remain in force. (2)The company law provisions of this Act are— (a)the provisions of Parts 1 to 39 of this Act, and (b)the provisions of Parts 45 to 47 of this Act so far as they apply for the purposes of those Parts. 1

Types of company 3 Limited and unlimited companies (1)A company is a “limited company” if the liability of its is limited by its constitution. It may be limited by shares or limited by guarantee. (2)If their liability is limited to the amount, if any, unpaid on the shares held by them, the company is “limited by shares”. (3)If their liability is limited to such amount as the undertake to contribute to the assets of the company in the event of its being wound up, the company is “limited by guarantee”. (4)If there is no limit on the liability of its , the company is an “unlimited company”. 4 Private and public companies (1)A “private company” is any company that is not a public company. (2)A “public company” is a company limited by shares or limited by guarantee and having a share capital— (a)whose certificate of incorporation states that it is a public company, and (b)in relation to which the requirements of this Act, or the former Companies Acts, as to registration or reregistration as a public company have been complied with on or after the relevant date. (3)For the purposes of subsection (2)(b) the relevant date is— (a)in relation to registration or re-registration in Great Britain, 22nd December 1980; (b)in relation to registration or re-registration in Northern Ireland, 1st July 1983. (4)For the two major differences between private and public companies, see Part 20. 5 Companies limited by guarantee and having share capital (1)A company cannot be formed as, or become, a company limited by guarantee with a share capital. (2)Provision to this effect has been in force— (a)in Great Britain since 22nd December 1980, and (b)in Northern Ireland since 1st July 1983. (3)Any provision in the constitution of a company limited by guarantee that purports to divide the company's undertaking into shares or interests is a provision for a share capital. This applies whether or not the nominal value or number of the shares or interests is specified by the provision. 6 Community interest companies (1)In accordance with Part 2 of the Companies (Audit, Investigations and Community Enterprise) Act 2004 (c. 27)— (a)a company limited by shares or a company limited by guarantee and not having a share capital may be formed as or become a community interest company, and (b)a company limited by guarantee and having a share capital may become a community interest company. (2)The other provisions of the Companies Acts have effect subject to that Part.

General 7 Method of forming company 2

(1)A company is formed under this Act by one or more persons— (a)subscribing their names to a memorandum of association (see section 8), and (b)complying with the requirements of this Act as to registration (see sections 9 to 13). (2)A company may not be so formed for an unlawful purpose. 8 Memorandum of association (1)A memorandum of association is a memorandum stating that the subscribers— (a)wish to form a company under this Act, and (b)agree to become of the company and, in the case of a company that is to have a share capital, to take at least one share each. (2)The memorandum must be in the prescribed form and must be authenticated by each subscriber. Requirements for registration 9 Registration documents (1)The memorandum of association must be delivered to the registrar together with an application for registration of the company, the documents required by this section and a statement of compliance. (2)The application for registration must state— (a)the company's proposed name, (b)whether the company's ed office is to be situated in England and Wales (or in Wales), in Scotland or in Northern Ireland, (c)whether the liability of the of the company is to be limited, and if so whether it is to be limited by shares or by guarantee, and (d)whether the company is to be a private or a public company. (3)If the application is delivered by a person as agent for the subscribers to the memorandum of association, it must state his name and address. (4)The application must contain— (a)in the case of a company that is to have a share capital, a statement of capital and initial shareholdings (see section 10); (b)in the case of a company that is to be limited by guarantee, a statement of guarantee (see section 11); (c)a statement of the company's proposed officers (see section 12). (5)The application must also contain— (a)a statement of the intended address of the company's ed office; and (b)a copy of any proposed articles of association (to the extent that these are not supplied by the default application of model articles: see section 20). (6)The application must be delivered— (a)to the registrar of companies for England and Wales, if the ed office of the company is to be situated in England and Wales (or in Wales); (b)to the registrar of companies for Scotland, if the ed office of the company is to be situated in Scotland; (c)to the registrar of companies for Northern Ireland, if the ed office of the company is to be situated in Northern Ireland. 10 Statement of capital and initial shareholdings 3

(1)The statement of capital and initial shareholdings required to be delivered in the case of a company that is to have a share capital must comply with this section. (2)It must state— (a)the total number of shares of the company to be taken on formation by the subscribers to the memorandum of association, (b)the aggregate nominal value of those shares, (c)for each class of shares— (i)prescribed particulars of the rights attached to the shares, (ii)the total number of shares of that class, and (iii)the aggregate nominal value of shares of that class, and (d)the amount to be paid up and the amount (if any) to be unpaid on each share (whether on of the nominal value of the share or by way of ). (3)It must contain such information as may be prescribed for the purpose of identifying the subscribers to the memorandum of association. (4)It must state, with respect to each subscriber to the memorandum— (a)the number, nominal value (of each share) and class of shares to be taken by him on formation, and (b)the amount to be paid up and the amount (if any) to be unpaid on each share (whether on of the nominal value of the share or by way of ). (5)Where a subscriber to the memorandum is to take shares of more than one class, the information required under subsection (4)(a) is required for each class. 11 Statement of guarantee (1)The statement of guarantee required to be delivered in the case of a company that is to be limited by guarantee must comply with this section. (2)It must contain such information as may be prescribed for the purpose of identifying the subscribers to the memorandum of association. (3)It must state that each member undertakes that, if the company is wound up while he is a member, or within one year after he ceases to be a member, he will contribute to the assets of the company such amount as may be required for— (a)payment of the debts and liabilities of the company contracted before he ceases to be a member, (b)payment of the costs, charges and expenses of winding up, and (c)adjustment of the rights of the contributories among themselves, not exceeding a specified amount.

12 Statement of proposed officers (1)The statement of the company's proposed officers required to be delivered to the registrar must contain the required particulars of— (a)the person who is, or persons who are, to be the first director or directors of the company; (b)in the case of a company that is to be a private company, any person who is (or any persons who are) to be the first secretary (or t secretaries) of the company; (c)in the case of a company that is to be a public company, the person who is (or the persons who are) to be the first secretary (or t secretaries) of the company. 4

(2)The required particulars are the particulars that will be required to be stated— (a)in the case of a director, in the company's of directors and of directors' residential addresses (see sections 162 to 166); (b)in the case of a secretary, in the company's of secretaries (see sections 277 to 279). (3)The statement must also contain a consent by each of the persons named as a director, as secretary or as one of t secretaries, to act in the relevant capacity. If all the partners in a firm are to be t secretaries, consent may be given by one partner on behalf of all of them. 13 Statement of compliance (1)The statement of compliance required to be delivered to the registrar is a statement that the requirements of this Act as to registration have been complied with. (2)The registrar may accept the statement of compliance as sufficient evidence of compliance. Registration and its effect 14 Registration If the registrar is satisfied that the requirements of this Act as to registration are complied with, he shall the documents delivered to him. 15 Issue of certificate of incorporation (1)On the registration of a company, the registrar of companies shall give a certificate that the company is incorporated. (2)The certificate must state— (a)the name and ed number of the company, (b)the date of its incorporation, (c)whether it is a limited or unlimited company, and if it is limited whether it is limited by shares or limited by guarantee, (d)whether it is a private or a public company, and (e)whether the company's ed office is situated in England and Wales (or in Wales), in Scotland or in Northern Ireland. (3)The certificate must be signed by the registrar or authenticated by the registrar's official seal. (4)The certificate is conclusive evidence that the requirements of this Act as to registration have been complied with and that the company is duly ed under this Act. 16 Effect of registration (1)The registration of a company has the following effects as from the date of incorporation. (2)The subscribers to the memorandum, together with such other persons as may from time to time become of the company, are a body corporate by the name stated in the certificate of incorporation. (3)That body corporate is capable of exercising all the functions of an incorporated company. (4)The status and ed office of the company are as stated in, or in connection with, the application for registration. (5)In the case of a company having a share capital, the subscribers to the memorandum become holders of the shares specified in the statement of capital and initial shareholdings. (6)The persons named in the statement of proposed officers— (a)as director, or 5

(b)as secretary or t secretary of the company, are deemed to have been appointed to that office. PART 38 COMPANIES: INTERPRETATION … Meaning of “subsidiary” and related expressions 1159 Meaning of “subsidiary” etc (1)A company is a “subsidiary” of another company, its “holding company”, if that other company— (a)holds a majority of the voting rights in it, or (b)is a member of it and has the right to appoint or remove a majority of its board of directors, or (c)is a member of it and controls alone, pursuant to an agreement with other , a majority of the voting rights in it, or if it is a subsidiary of a company that is itself a subsidiary of that other company. (2)A company is a “wholly-owned subsidiary” of another company if it has no except that other and that other's wholly-owned subsidiaries or persons acting on behalf of that other or its wholly-owned subsidiaries. (3)Schedule 6 contains provisions explaining expressions used in this section and otherwise supplementing this section. (4)In this section and that Schedule “company” includes any body corporate.

The Partnership Act 1890 Nature of Partnership 1 Definition of partnership. (1) Partnership is the relation which subsists between persons carrying on a business in common with a view of profit. (2)But the relation between of any company or association which is— (a)ed as a company under the Companies Act 1862, or any other Act of Parliament for the time being in force and relating to the registration of t stock companies; or (b)Formed or incorporated by or in pursuance of any other Act of Parliament or letters patent, or Royal Charter; is not a partnership within the meaning of this Act. 2 Rules for determining existence of partnership. In determining whether a partnership does or does not exist, regard shall be had to the following rules: (1)t tenancy, tenancy in common, t property, common property, or part ownership does not of itself create a partnership as to anything so held or owned, whether the tenants or owners do or do not share any profits made by the use thereof.

6

(2)The sharing of gross returns does not of itself create a partnership, whether the persons sharing such returns have or have not a t or common right or interest in any property from which or from the use of which the returns are derived. (3)The receipt by a person of a share of the profits of a business is primâ facie evidence that he is a partner in the business, but the receipt of such a share, or of a payment contingent on or varying with the profits of a business, does not of itself make him a partner in the business; and in particular— (a)The receipt by a person of a debt or other liquidated amount by instalments or otherwise out of the accruing profits of a business does not of itself make him a partner in the busines or liable as such: (b)A contract for the remuneration of a servant or agent of a person engaged in a business by a share of the profits of the business does not of itself make the servant or agent a partner in the business or liable as such: (c)A person being the widow or child of a deceased partner, and receiving by way of annuity a portion of the profits made in the business in which the deceased person was a partner, is not by reason only of such receipt a partner in the business or liable as such: (d)The advance of money by way of loan to a person engaged or about to engage in any business on a contract with that person that the lender shall receive a rate of interest varying with the profits, or shall receive a share of the profits arising from carrying on the business, does not of itself make the lender a partner with the person or persons carrying on the business or liable as such. Provided that the contract is in writing, and signed by or on behalf of all the parties thereto: (e)A person receiving by way of annuity or otherwise a portion of the profits of a business in consideration of the sale by him of the goodwill of the business is not by reason only of such receipt a partner in the business or liable as such. 3 Postponement of rights of person lending or selling in consideration of share of profits in case of insolvency. In the event of any person to whom money has been advanced by way of loan upon such a contract as is mentioned in the last foregoing section, or of any buyer of a goodwill in consideration of a share of the profits of the business, being adjudged a bankrupt, entering into an arrangement to pay his creditors less than in the pound, or dying in insolvent circumstances, the lender of the loan shall not be entitled to recover anything in respect of his loan, and the seller of the goodwill shall not be entitled to recover anything in respect of the share of profits contracted for, until the claims of the other creditors of the borrower or buyer for valuable consideration in money or money’s worth have been satisfied.

4 Meaning of firm. (1)Persons who have entered into partnership with one another are for the purposes of this Act called collectively a firm, and the name under which their business is carried on is called the firm-name. (2)In Scotland a firm is a legal person distinct from the partners of whom it is composed, but an individual partner may be charged on a decree or diligence directed against the firm, and on payment of the debts is entitled to relief pro ratâ from the firm and its other . 5 Power of partner to bind the firm. Every partner is an agent of the firm and his other partners for the purpose of the business of the partnership; and the acts of every partner who does any act for carrying on in the usual way business of the kind carried on by the firm of which he is a member bind the firm and his partners, unless the partner so acting has in fact no authority to act for the firm in the particular matter, and the person with whom he is dealing either knows that he has no authority, or does not know or believe him to be a partner. 9 Liability of partners. 7

Every partner in a firm is liable tly with the other partners, and in Scotland severally also, for all debts and obligations of the firm incurred while he is a partner; and after his death his estate is also severally liable in a due course of istration for such debts and obligations, so far as they remain unsatisfied, but subject in England or Ireland to the prior payment of his separate debts.

The Limited Partnership Act 1907 4 Definition and constitution of limited partnership. (1) limited partnerships may be formed in the manner and subject to the conditions by this Act provided. (2)A limited partnership must consist of one or more persons called general partners, who shall be liable for all debts and obligations of the firm, and one or more persons to be called limited partners, who shall at the time of entering into such partnership contribute thereto a sum or sums as capital or property valued at a stated amount, and who shall not be liable for the debts or obligations of the firm beyond the amount so contributed. (3)A limited partner shall not during the continuance of the partnership, either directly or indirectly, draw out or receive back any part of his contribution, and if he does so draw out or receive back any such part shall be liable for the debts and obligations of the firm up to the amount so drawn out or received back. (4)A body corporate may be a limited partner. 6 Modifications of general law in case of limited partnerships. (1)A limited partner shall not take part in the management of the partnership business, and shall not have power to bind the firm: Provided that a limited partner may by himself or his agent at any time inspect the books of the firm and examine into the state and prospects of the partnership business, and may advise with the partners thereon. If a limited partner takes part in the management of the partnership business he shall be liable for all debts and obligations of the firm incurred while he so takes part in the management as though he were a general partner. (2)A limited partnership shall not be dissolved by the death or bankruptcy of a limited partner, and the lunacy of a limited partner shall not be a ground for dissolution of the partnership by the court unless the lunatic’s share cannot be otherwise ascertained and realised. (3)In the event of the dissolution of a limited partnership its affairs shall be wound up by the general partners unless the court otherwise orders. (4) (5)Subject to any agreement expressed or implied between the partners— (a)Any difference arising as to ordinary matters connected with the partnership business may be decided by a majority of the general partners; (b)A limited partner may, with the consent of the general partners, assign his share in the partnership, and upon such an assignment the assignee shall become a limited partner with all the rights of the assignor; (c)The other partners shall not be entitled to dissolve the partnership by reason of any limited partner suffering his share to be charged for his separate debt; (d)A person may be introduced as a partner without the consent of the existing limited partners; (e)A limited partner shall not be entitled to dissolve the partnership by notice.

The Limited Liability Partnerships Act 2000 8

1 Limited liability partnerships. (1)There shall be a new form of legal entity to be known as a limited liability partnership. (2)A limited liability partnership is a body corporate (with legal personality separate from that of its ) which is formed by being incorporated under this Act; and— (a)in the following provisions of this Act (except in the phrase “oversea limited liability partnership”), and (b)in any other enactment (except where provision is made to the contrary or the context otherwise requires), references to a limited liability partnership are to such a body corporate. (3)A limited liability partnership has unlimited capacity. (4)The of a limited liability partnership have such liability to contribute to its assets in the event of its being wound up as is provided for by virtue of this Act. (5)Accordingly, except as far as otherwise provided by this Act or any other enactment, the law relating to partnerships does not apply to a limited liability partnership. (6)The Schedule (which makes provision about the names and ed offices of limited liability partnerships) has effect. 6 as agents. (1)Every member of a limited liability partnership is the agent of the limited liability partnership. (2)But a limited liability partnership is not bound by anything done by a member in dealing with a person if— (a)the member in fact has no authority to act for the limited liability partnership by doing that thing, and (b)the person knows that he has no authority or does not know or believe him to be a member of the limited liability partnership. (3)Where a person has ceased to be a member of a limited liability partnership, the former member is to be regarded (in relation to any person dealing with the limited liability partnership) as still being a member of the limited liability partnership unless— (a)the person has notice that the former member has ceased to be a member of the limited liability partnership, or (b)notice that the former member has ceased to be a member of the limited liability partnership has been delivered to the registrar. (4)Where a member of a limited liability partnership is liable to any person (other than another member of the limited liability partnership) as a result of a wrongful act or omission of his in the course of the business of the limited liability partnership or with its authority, the limited liability partnership is liable to the same extent as the member.

Promoters: An individual who persuades others to invest capital to a company to be incorporated for the purpose of carrying on a venture. A person who solicits people to invest money into a corporation, usually when it is being formed. An investment banker, an underwriter, or a stock promoter may, wholly or in part, perform the role of a promoter. Promoters generally owe a duty of utmost good faith, so as to not mislead any potential investors, and disclose all material facts about the company's business. A promoter is a person who does the preliminary work incidental to the formation of company. 9

The primary remedy for breach of fiduciary obligation by a promoter is “an of profits (sometimes referred to as an ing for profits or simply an ing) is a type of equitable remedy most commonly used in cases of breach of fiduciary duty. It is an action taken against a defendant to recover the profits taken as a result of the breach of duty, in order to prevent unjust enrichment. Twycross v Grant (1877): A promoter, I apprehend is one who undertakes to form of a company with reference to a given project and to set it going, and who takes the necessary steps to accomplish that purpose…and so long as the work of formation continues, those who carry on that work must, I think, retain the character of promoters. Of course, if a governing body, in the shape of directors, has once been formed, and they take…what remains to be done in the way of forming the company, into their hands, the functions of the promoter are at an end. Erlanger v New Sombrero Phosphate Co (1878) [Fiduciary Duty]: “The have in their hands the creation and moulding of the company; they have the power of defining how, and when, and in what shape, and under what supervision, it shall start into existence and begin to act as a trading corporation.” A promoter’s undisclosed profit is usually called a ‘secret profit’; failure to disclose the interest of the company’s promoter in a transaction with the company is voidable at the company’s option. The company may rescind the transaction. Gluckstein v Barnes [1900]: Mr Gluckstein and others formed a syndicate to promote a company. They purchased a (Olympia) hall for the price of 120,000.00, but the prospectus (for the public) gave the impression they had actually paid 140,000. Macnaghten L found this to be dishonest and Mr Gluckstein (the only promoter proceeded against) was ordered to pay the company his share of the profit. [Because the fiduciary relationship/duty of the Promoter does not exist in Statute, and exists only in Equity, one must apply maxims in order to determine if a wrong has transpired] *A promoter usually makes money by selling an asset to the company at an enhanced price, and then disclosing that profit. If not, the promoter may be subject to repay this profit. Alternatively, if the asset was purchased many years prior to the deal and with no intention to sell to the company then those profits [are personal] and need not be disclosed. *A promoter cannot enter into a contract with the company (and be paid through agreement/contract) as the company has yet to be formed and “Past Consideration is Not Good Consideration”. That said, the promoters can be paid through the company’s Constitution – but this is unsafe if they do not control the board (as they will have no power over levels of remuneration).

Pre-Incorporation Contracts: Companies Act 2006 s.51: 51 Pre-incorporation contracts, deeds and obligations (1)A contract that purports to be made by or on behalf of a company at a time when the company has not been formed has effect, subject to any agreement to the contrary, as one made with the person purporting to act for the company or as agent for it, and he is personally liable on the contract accordingly. (2)Subsection (1) applies— 10

(a)to the making of a deed under the law of England and Wales or Northern Ireland, and (b)to the undertaking of an obligation under the law of Scotland, as it applies to the making of a contract. Two possibilities: 1) Either, pursuant to s.51 above, the person acting as agent for the anticipated company is personally liable (Kelner v Baxter (1866) – Guy buys wine for hotel which has yet to incorporate; wine supplier sues principle (company) claiming that entrepreneur is acting as agent for the principle; judge however finds entrepreneur liable as principle); or a. A person may avoid liability by entering into an ‘agreement to the contrary’ – though this concept was rejected by the CoA. 2) The contract is between the contractor and the company, in which case, the company being nonexistent, there is no contract and no one is liable. (Newborne v Sensolid (Great Britain) Ltd [1954] – Mr. Newborne, founder of intended company, as it was, signed contract for purchasing equipment in companies’ name.) a. Position depends on INTENTION of parties at contract formation (Phonogram Ltd v Lane [1982]). It was suggested that, for the purposes of s 51(1), a contract is ‘purported’ to be made by a company only when there has been a representation that the company is already in existence. i. Promoters are now personally liable in respect of pre-incorporation contracts made for the benefit of the unformed company, irrespective of the capacity in which they purport to contract and irrespective of their subjective beliefs. b. It makes no difference that the shelf company (a company with no activity) did not have the right name at the time the contracts were made (Oshkosh B’Gosh Inc v Dan Marbel Inc Ltd. [1989] – s.51 Held not to apply) Novation: “What may be provided in a pre-incorporation contract is that the person making it will be released from liability on it if the company, after incorporation, enters into a second contract with the contractor in the same as the pre-incorporation contract.

Registration/Incorporation: In the UK, a company is created by ing it with a government agency call Companies House (the executive agency of the Department of Business, Innovation and Skills). www.companieshouse.gov.uk The Chief Executive of the Companies House is the registrar of companies. To a company you must have at least ‘2’ .

11

Lecture #3: Corporate Personality and the Veil of Incorporation Piercing the Corporate Veil: It’s when the courts ignore the concept of the company having a ‘separate corporate personality’ and find the individual responsible. On page 127 there is a more precise definition: ‘Where the Courts ignore the separate legal personality and treat a company’s property, rights and obligations as belonging to a person who owns and controls the company’. There is probably only one circumstance in which veil piercing is possible: where it is necessary in order to apply the evasion principle. Salomon v A Salomon & Co Ltd [1897] AC 22 Landmark UK company law case. The effect of the Lords' unanimous ruling was to uphold firmly the doctrine of corporate personality, as set out in the Companies Act 1862, so that creditors of an insolvent company could not sue the company's shareholders to pay up outstanding debts. Salomon conducted his business as a sole trader (owning a shoe company). He sold it to a company incorporated for the purpose called A Salomon and Co Ltd (advised by solicitor to “sell business” to an incorporated company – at this time the requirement was that there be 7 ). The only were Mr Salomon, his wife, and their five children. Each member took one £1 share each. The company bought the business for £39,000. Mr Salomon subscribed for 20,000 further shares. However, £10,000 was not paid by the company, which instead issued Salomon with series of debentures (with a security device – the factory) and gave him a floating charge (v fixed charge) on its assets. £8,993 was paid to Mr Salomon in cash. When the company failed the company's liquidator contended that the floating charge should not be honoured, and Salomon should be made responsible for the company's debts. (Raw materials, ie, leather and coal, were supplied to Mr Salomon by Trade Creditors, later sold to the Company.) Upon sale, Mr. Salomon is no longer the owner, but becomes the director (manager and major shareholder with 20,001 shares, and the owner of the debenture). The ‘floating charge’ attaches to all assets of the company, and anything of value: acts as a security device upon insolvency of company giving priority to debenture (floating charge) holder. Lord Halsbury LC stated (at 30-31): “… it seems to me impossible to dispute that once the company is legally incorporated it must be treated like any other independent person with its rights and liabilities appropriate to itself, and that the motives of those who took part in the promotion of the company are absolutely irrelevant in discussing what those rights and liabilities are.” From this case comes the fundamental concept that a company has a legal personality or identity separate from its . A company is thus a legal ‘person'. As long as the company has filed the requisite documents and has been ed via Companies House (compliance with the Rules), they become a separate identity. In the instant case, after establishing there was a bona fide, properly incorporated company, they would examine whether the debenture was issued correctly – which it had. At first instance under heading Broderip v Salomon [1895] it was held that the company conducted the business as agent for Mr. Salomon, so he was responsible for all debts incurred in the course of the agency for him. The HoL’s rejected this approach. At the CoA, under the same heading, it was held that Mr. Salomon had incorporated contrary to the ‘true intent’ and meaning of CA 1862, and because of Mr. Salomon’s fraud, the company should be declared to have operated the business as trustee for Mr. Salomon, who should therefore indemnify the company for all debts incurred in carrying out the trust. (In a trust, if the trustee loses the property, the beneficiary is entitled to sue for the full amount of that loss). The HoL’s also rejected this argument. 12

Debenture: is a medium- to long-term debt instrument used by large companies to borrow money, at a fixed rate of interest. The legal term "debenture" originally referred to a document that either creates a debt or acknowledges it, but in some countries the term is now used interchangeably with bond, loan stock or note. A debenture is thus like a certificate of loan or a loan bond evidencing the fact that the company is liable to pay a specified amount with interest and although the money raised by the debentures becomes a part of the company's capital structure, it does not become share capital. Senior debentures get paid before subordinate debentures, and there are varying rates of risk and payoff for these categories. Debentures are generally freely transferable by the debenture holder. Debenture holders have no rights to vote in the company's general meetings of shareholders, but they may have separate meetings or votes e.g. on changes to the rights attached to the debentures. The interest paid to them is a charge against profit in the company's financial statements.

Floating charge: is a security interest over a fund of changing assets of a company or a limited liability partnership (LLP), which 'floats' or 'hovers' until the point at which it is converted into a fixed charge, at which point the charge attaches to specific assets of the company or LLP. This conversion into a fixed charge (called "crystallisation") can be triggered by a number of events; inter alia, it has become an implied term (under English law) in debentures that a cessation of the company's right to deal with the assets in the ordinary course of business leads to automatic crystallisation. Additionally, according to express of a typical loan agreement, default by the chargor is a trigger for crystallisation. Such defaults typically include non-payment, invalidity of any of the lending or security documents or the launch of insolvency proceedings. Floating charges can only be granted by companies or LLPs. If an individual person or a partnership was to purport to grant a floating charge, it would be void as a general assignment in bankruptcy. Floating charges take effect in equity only, and consequently are defeated by a bona fide purchaser for value without notice of any asset covered by them. In practice, as the chargor has power to dispose of assets subject to a floating charge, this is only of consequence in relation to disposals that occur after the charge has crystallised. The floating charge has been described as "one of equity's most brilliant creations."

The Corporate Veil: Pg 127: Can the court ignore the separation between the separate legal personality and treat a company’s property, rights and obligations as belonging to a person who owns and controls the company. This has been called ‘piercing the corporate veil’. There are specific legal principles that can be used to attribute one person’s property to another person, whether the persons are natural or legal: 1) Statutory; 2) Contract; 3) Agency; 4) Trustee. 1) Statutory Provisions: The separate personality of a company is created by a statute, CA 2006, and can be modified by other statutes, for example, Landlord and Tenant Act 1954, s30, the Inheritance Tax Act 1984, Inheritance Act 1986 s. 213. “…it is submitted that these provisions to not represent a desire on the part of the legislature to disregard the company’s separate personality, but merely impose additional liability on those responsible for the expression of the corporate personality in these circumstances.” (pg 129) 13

2) Contract: Nothing in company law prevents a person from contracting out of any benefit the person could derive from the principle of separate corporate personality. 3) Agency: Principle – Agent relationship is a question of fact, and agency can be inferred from the surrounding circumstances, though it can only be established by the consent of the principle and the agent. The liability arises under agency law, and not company law. Agency cannot be inferred, however, from the control exercisable by the over the company – either by virtue of their votes in general meeting or because they are also directors – or from the fact that the sole objective of the company is to benefit the . (Smith Stone Knight Ltd v Birmingham Corp [1939]) 4) Property held in Trust: Prest v Petrodel Resources Ltd UKSC [2013] (Pg 128): Mrs Yasmin Prest claimed under Matrimonial Causes Act 1973 sections 23 and 24 for ancillary relief against the offshore companies solely owned by Mr Michael Prest. Mrs Prest said they held legal title to properties that he beneficially owned, including a £4m house at 16 Warwick Avenue, London. They had married in 1993 and divorced in 2008. He did not comply with orders for full and frank disclosure of his financial position, and the companies did not file a defence. The Matrimonial Causes Act 1973 section 24 required that for a court to be able to order a transfer a property, Mr Prest had to be ‘entitled’ to the properties held by his companies. Mr Prest contended that he was not entitled to the properties. The SC heard three arguments: 1) no relevant impropriety therefore not entitled to pierce corporate veil; 2) Court could not claim special (or wider) jurisdiction under Matrimonial Act (but under evidence) 3) Mr Prest had been beneficial owner of property and therefore held on trust. SC held, unanimously, that piercing the corporate veil could not be used to treat the companies’ assets as belonging to Mr. Prest as there was no impropriety. However, the evidence showed that the companies held the properties as a trustee for Michael Prest, not simply because he was the owner and controller of the companies, but because of the circumstances in which the properties were acquired by the companies.

Lord Sumpton in Prest at para 28: The difficulty is to identify what is a relevant wrongdoing. References to a “facade” or “sham” beg too many questions to provide a satisfactory answer. It seems to me that two distinct principles lie behind these protean , and that much confusion has been caused by failing to distinguish between them. They can conveniently be called the concealment principle and the evasion principle. The concealment principle is legally banal and does not involve piercing the corporate veil at all. It is that the interposition of a company or perhaps several companies so as to conceal the identity of the real actors will not deter the courts from identifying them, assuming that their identity is legally relevant. In these cases the court is not disregarding the “facade”, but only looking behind it to discover the facts which the corporate structure is concealing. The evasion principle is different. It is that the court may disregard the corporate veil if there is a legal right against the person in control of it which exists independently of the company’s involvement, and a company is interposed so that the separate legal personality of the company will defeat the right or frustrate its enforcement. Many cases will fall into both categories, but in some circumstances the difference between them may be critical. This may be illustrated by reference to those cases in which the court has been thought, rightly or wrongly, to have pierced the corporate veil. Concealment Principle: when a company is used as a device or façade to conceal the true facts and avoid or conceal the liability of the individual controlling the company (e.g. Prest v Petrodel Resources Ltd 14

[2013]). In that vein, the interposition of a company or perhaps several companies so as to conceal the identity of the real actors will not deter the courts from identifying them, assuming that their identity is legally relevant. In these cases the courts is not disregarding the ‘façade’, but only looking behind it to discover the facts which the corporate structure is concealing. Evasion Principle (pg 134): When an individual interposes a company so as to evade, or frustrate the enforcement of, an existing legal obligation, liability or restriction. In this scenario, rather than looking behind the façade, here the Courts disregard the corporate veil, depriving the company or its controller of the advantage that they would otherwise have obtained by the company’s separate legal personality. (Eg Jones v Lipman)

Gilford Motors Ltd. v Horne [1933] ch 935 Facts: Mr EB Horne was formerly a managing director of the Gilford Motor Co Ltd. His employment contract stipulated (clause 9) not to solicit customers of the company if he were to leave employment of Gilford Motor Co. Mr. Horne was fired, thereafter he set up his own business and undercut Gilford Motor Co's prices. He received legal advice saying that he was probably acting in breach of contract. So he set up a company, JM Horne & Co Ltd, in which his wife and a friend called Mr Howard were the sole shareholders and directors. They took over Horne’s business and continued it. Mr. Horne sent out fliers saying, Spares and service for all models of Gilford vehicles. 170 Hornsey Lane, Highgate, N.6. Opposite Crouch End Lane…No connection with any other firm. The company had no such agreement with Gilford Motor about not competing, however Gilford Motor brought an action alleging that the company was used as an instrument of fraud to conceal Mr Horne's illegitimate actions.

Jones v Lipman [1962] 1 WLR 832 [Evasion Principle] (Pg 134) The defendant had contracted to sell his land. He changed his mind, and formed a company of which he was owner and director, transferred the land to the company, and refused to complete. The plaintiff sought relief. Held: Specific performance is available against a contracting vendor who has it in his power to compel another person to convey the property in question. An order for specific performance was made against both the director and the company. The company could not escape from or divest itself of its knowledge gained through the director. The company was: ‘A creature of [the controlling director], a device and a sham, a mask which he holds before his face in an attempt to avoid recognition by the eye of equity.’ Parent v subsidiary distinction: sometimes ‘risky’ investments are placed in the subsidiary in the event that this company runs up debts which they are unable to pay the parent company simply allows that subsidiary to become insolvent, as the parent company remains intact. Subsidiary: A company whose voting stock is more than 50% controlled by another company, usually referred to as the parent company or holding company. A subsidiary is a company that is partly or completely owned by another company that holds a controlling interest in the subsidiary company. If a parent company owns a foreign subsidiary, the company under which the subsidiary is incorporated must 15

follow the laws of the country where the subsidiary operates, and the parent company still carries the foreign subsidiary's financials on its books (consolidated financial statements). For the purposes of liability, taxation and regulation, subsidiaries are distinct legal entities.

DNH Foods v. London Borough of Tower Hamlets [1976] WLR 852 [Subsidiaries – Evasion Principle – Group Entity/Single Entity] LBTH made a ‘compulsory purchase’ of land in which ‘Golden Foods’ operated – which was a subsidiary of DNH Foods. Under the legislation compensation was to be paid: whatever the value of the land. However, the parent company, DNH Foods, carried on some of its business at this Golden Foods location, which the legislation did not address. CoA Lord Denning: ‘Group Entity’ – if part of entity is damaged, all the parts that are damaged must be compensated. Prof. Ryan suggests this is not a ‘lifting of a veil’ but rather ‘piercing the veil’ – which is different. The positive public reception was short-lived as the distinction between the parent and subsidiary was muddied… “A company may operate its business in separate branches at geographically separate locations. It is possible for a company to incorporate separate companies, as subsidiaries, to operate each branch and each of those subsidiaries will be a separate legal person. If that is not done, company law does not treat each branch as a separate person, even if it is in another country: instead there is just one legal person operating the whole business.” (pg 124 MF&R)

**Adams v Cape Industries Plc [1990] ch 433 [Subsidiaries]**(READ PG 143) Facts: The defendant was an English company and head of a group engaged in mining asbestos in South Africa. A wholly owned English subsidiary was the worldwide marketing body, which protested the jurisdiction of the United States Federal District Court in Texas in a suit by victims of asbestos. The defendant took no part in the United States proceedings and default judgments were entered. Actions on the judgment in England failed. [Question: Should parent company be liable for actions/debts of subsidiaries (in the instant case, the default judgment against it)? Three arguments advanced: (1) this is a group entity; and (2) the subsidiary was an agent for the parent. If there is a contract of ‘agency’ between them, or by implication, the latter argument may be accepted. (3) The last argument advanced was that the Company was a sham/facade (entity), and so not a separate legal entity. All three arguments were rejected] Held: The court declined to pierce the veil of incorporation. It was a legitimate use of the corporate form to use a subsidiary to insulate the remainder of the group from tort liability. There was no evidence to justify a finding of agency or facade. There is an exception to the general rule, that steps which would not have been regarded by the domestic law of the foreign court as a submission to the jurisdiction ought not to be so regarded here, notwithstanding that if they had been steps taken in an English Court they might have constituted a submission to jurisdiction.

16

Slade LJ said: ‘Two points at least are clear. First, at common law in this country foreign judgments are enforced, if at all, not through considerations of comity but upon the basis of the principle explained thus by Parke B. in Williams v Jones. Secondly, however, in deciding whether the foreign court was one of competent jurisdiction, our courts will apply not the law of the foreign court itself but our own rules of private international law. .’ and ‘First, in determining the jurisdiction of the foreign court in such cases, our court is directing its mind to the competence or otherwise of the foreign court ‘to summon the defendant before it and to decide such matters as it has decided:’ see Pemberton v Hughes [1899] 1 Ch. 781, 790 per Lindley M.R. Secondly, in the absence of any form of submission to the foreign court, such competence depends on the physical presence of the defendant in the country concerned at the time of suit... we would, on the basis of the authorities referred to above, regard the source of the territorial jurisdiction of the court of a foreign country to summon a defendant to appear before it as being his obligation for the time being to abide by its laws and accept the jurisdiction of its courts while present in its territory. So long as he remains physically present in that country, he has the benefit of its laws, and must take the rough with the smooth, by accepting his amenability to the process of its courts.’ [*Must Read Judgment, in particular, Lord Slade’s reasoning, and why he did not find the ‘group entity’ argument convincing] Following this decision, more miners were diagnosed with asbestosis, and before litigation commenced, the parent company dissolved the subsidiary. Instead of trying the case in South Africa, the HoL’s, rather surprisingly, allowed the matter to be heard in front of them. Before the trial commenced Cape Industries settled, fearing the corporate veil would be lifted. Bank of Montreal v Canadian Westgrove Ltd (1990): demonstrates an incredibly high threshold for a finding of Parent company liability for (contractual relations) made by a wholly owned subsidiary. The CoA stated that “one would need pretty clear – possibly overwhelming – evidence of agency or something else.” (Pg 145)

Smith Stone Knight Ltd v Birmingham Corp [1939] 4 ALL ER 116 [Company carrying on business as agent of its – agency through implication - SUFFICIENT CONTROL] (Pg 131) Facts: An application was made to set aside a preliminary determination by an arbitrator. The parties disputed the compensation payable by the respondent for the acquisition of land owned by Smith Stone and held by Birmingham Waste as its tenant on a yearly tenancy. Birmingham Waste was a wholly owned subsidiary of Smith Stone and was said in the Smith Stone claim to carry on business as a separate department and agent for Smith Stone. As a yearly tenant, Birmingham Waste, however, had no status to claim compensation. The question was whether, as a matter of law, the parent company could claim compensation for disturbance to the business carried on at the acquired premises. The arbitrator’s award answered this in the negative. Smith Stone applied to set the award aside on the ground of technical misconduct. Held: An implied agency existed between the parent and subsidiary companies so that the parent was considered to own the business carried on by the subsidiary and could claim compensation for disturbance caused to the subsidiary’s business by the local council. In determining whether a subsidiary was an implied agent of the parent, Atkinson J examined whether, on the facts as found by the arbitrator and after rejecting certain conclusions of fact which were uned by evidence, Smith Stone was in fact the real owner of 17

the business and was therefore entitled to compensation for its disturbance. Accordingly, the parent company was entitled to compensation both for the value of land and for disturbance of the business because it owned both the land and the business. The rule to protect the fact of separate corporate identities was circumvented because the subsidiary was the agent, employee or tool of the parent. The subsidiary company was operating a business on behalf of its parent company because its profits were treated entirely as those of the parent company’s; it had no staff and the persons conducting the business were appointed by the parent company, and it did not govern the business or decide how much capital should be embarked on it. In those circumstances, the court was able to infer that the company was merely the agent or nominee of the parent company. Atkinson J formulated six relevant criteria, namely: (a) Were the profits treated as profits of the parent? (b) Were the persons conducting the business appointed by the parent? (c) Was the parent the head and brain of the trading venture? (d) Did the parent govern the venture, decide what should be done and what capital should be embarked on the venture? (e) Did the parent make the profits by its skill and direction? (f) Was the parent in effectual and constant control?’

In Yukong Lind Ltd v Rendsburg Investments Corp. [1998] Toulson J rejected the submission that these points should determine whether a company is carrying on business as another person’s agent.

Chandler v Cape Plc [2012] EWCA Civ 525 [Tortious Liability] The Court of Appeal has upheld a decision of the High Court which found that a parent company owed a direct duty of care to an employee of one of its subsidiaries.(This case is not about lifting the Corporate Veil – this is about finding liability for negligence re Cape (parent) undertaking to regulate the Health & Safety across its subsidiaries) In this case, the claimant, Mr Chandler, was employed by a subsidiary of Cape plc for just over 18 months from 1959 to 1962. During the course of his employment, Mr Chandler was exposed to asbestos fibres and in 2007 Mr Chandler was diagnosed with asbestosis. By this time, the subsidiary entity had been dissolved. Mr Chandler’s estate brought a claim against Cape plc alleging it had owed (and breached) a duty of care to Mr Chandler. It was held at first instance that Cape plc owed Mr Chandler a duty of care. Cape plc appealed, but its appeal was dismissed. The key points to note are as follows: The Court of Appeal stated that Cape plc assumed responsibility to Mr Chandler and owed a direct duty of care to Mr Chandler which it breached. The Court of Appeal stressed that the duty of care from a parent company to subsidiary employees did not exist automatically and only arose in particular circumstances. That is, there was no imposition or assumption of responsibility to the employee by reason only that the defendant was the parent company: parent companies have a separate legal personality and it should, as a rule, not be possible to “pierce the corporate veil”. However, in the case of Cape plc, the Court of Appeal identified parallel duties of care between the parent company and subsidiary employees and the subsidiary company and its employees. This was because: (i) the parent company and subsidiary had relatively similar businesses; 18

(ii) (iii) (iv)

the parent has, or ought to have, superior knowledge on some relevant aspect of health and safety in the particular industry; the subsidiary’s system of work is unsafe as the parent company knew, or ought to have known; the parent company knew (or ought to have foreseen) that the subsidiary or its employees would rely on its using that superior knowledge the employees’ protection.

The case results in case law catching up with the group/subsidiary corporate structures that are now relatively common. It is likely that courts will look at group structures holistically. Moreover, the country of incorporation of a subsidiary is unlikely to make a difference if the parent entity is a UK plc. In particular, in the case of M&A transactions involving the sale or purchase of a subsidiary entity, parties will need to think about contingent and residual liability issues arising for parent companies. Daimler AG v Bauman et al [2013] [Parent-Subsidiary liability; Extra-territorial jurisdiction] Plaintiffs (respondents here) are twenty-two residents of Argentina who filed suit in California Federal District Court, naming as a defendant DaimlerChrysler Aktiengesellschaft (Daimler), a German public stock company that is the predecessor to petitioner Daimler AG. Their complaint alleges that Mercedes-Benz Argentina (MB Argentina), an Argentinian subsidiary of Daimler, collaborated with state security forces during Argentina’s 1976–1983 “Dirty War” to kidnap, detain, torture, and kill certain MB Argentina workers, among them, plaintiffs or persons closely related to plaintiffs. Based on those allegations, plaintiffs asserted claims under the Alien Tort Statute and the Torture Victim Protection Act of 1991, as well as under California and Argentina law. Personal jurisdiction over Daimler was predicated on the California s of Mercedes-Benz USA, LLC (MBUSA), another Daimler subsidiary, one incorporated in Delaware with its principal place of business in New Jersey. MBUSA distributes Daimler-manufactured vehicles to independent dealerships throughout the United States, including California. Daimler moved to dismiss the action for want of personal jurisdiction. Opposing that motion, plaintiffs argued that jurisdiction over Daimler could be founded on the California s of MBUSA. The District Court granted Daimler’s motion to dismiss. Reversing the District Court’s judgment, the Ninth Circuit held that MBUSA, which it assumed to fall within the California courts’ all-purpose jurisdiction, was Daimler’s “agent” for jurisdictional purposes, so that Daimler, too, should generally be answerable to suit in that State. Held: Daimler is not amenable to suit in California for injuries allegedly caused by conduct of MB Argentina that took place entirely outside the United States. Today, the Supreme Court of the United States held in Daimler AG v. Bauman, et al. that due process prevents a court from applying an "agency" theory to exercise general personal jurisdiction over a foreign corporation based solely on unrelated s of its domestic, wholly-owned subsidiary, if the subsidiary is not otherwise an alter ego of the parent corporation. Justice Ginsburg delivered the opinion of the Court, in which Chief Justice Roberts and Justices Scalia, Kennedy, Thomas, Breyer, Alito and Kagan ed. Justice Sotomayor wrote a concurring opinion. The Court's ruling reversed a 2011 decision of Judge Stephen Reinhardt of the United States Court of Appeals for the Ninth Circuit. The Court held that the Ninth Circuit’s two-part "agency" test did not satisfy the requirements of due process. Under the Ninth Circuit test, a court could exercise general personal jurisdiction over a foreign parent corporation for activities that occurred entirely outside of the U.S. if (1) it would perform the tasks of the subsidiary if the subsidiary did not exist and (2) it had the “right to control” the subsidiary. Applying this test, the Ninth Circuit had held that the foreign parent (the corporate predecessor to Daimler AG) would perform all the tasks of its domestic subsidiary, Mercedes Benz USA, i.e., selling cars in the American market, if the subsidiary did not exist, and that the parent had the right to control virtually every function of the domestic subsidiary. Thus, the Ninth Circuit held that it could exercise general personal jurisdiction over the foreign parent based on the activities of its subsidiary in California. 19

The Supreme Court rejected the Ninth's Circuit's "agency" test for general personal jurisdiction. The Court found that the "Ninth Circuit's agency theory … appears to subject foreign corporations to general jurisdiction whenever they have an in-state subsidiary or , an outcome that would sweep beyond even the 'sprawling view of general jurisdiction'" that the Court previously rejected in its decision in Goodyear Dunlop Tires Operations, S.A. v. Brown, 564 U.S. __ (2011). The Court noted that "[i]f Daimler's California activities sufficed to allow adjudication of this Argentina-rooted case in California, the same global reach would presumably be available in every other State in which MBUSA's sales are sizable. Such exorbitant exercises of all-purpose jurisdiction would scarcely permit out-of-state defendants 'to structure their primary conduct with some minimum assurance as to where that conduct will and will not render them liable to suit.'" The Court concluded that "[i]t was therefore error for the Ninth Circuit to conclude that Daimler, even with MBUSA's s attributed to it, was at home in California, and hence subject to suit there on claims by foreign plaintiffs having nothing to do with anything that occurred or had its principal impact in California." The Court also emphasized the transnational context of the dispute in reaching its holding, and found that the Ninth's Circuit's decision "paid little heed to the risks to international comity its expansive view of general jurisdiction posed…. Considerations of international rapport thus reinforce our determination that subjecting Daimler to the general jurisdiction of courts in California would not accord with the 'fair play and substantial justice' due process demands." Choc v HudBay Minerals Inc. & Caal v HudBay Minerals Inc. [2013] [Parent-Subsidiary liability; Extra-territorial jurisdiction] Agency & Façade arguments advanced in Canadian cases, but not Group-Entity of the indigenous Mayan Q’eqchi’ population from El Estor, Guatemala have filed three related lawsuits in Ontario courts against Canadian mining company HudBay Minerals over the brutal killing of Adolfo Ich, the gang-rape of 11 women from Lote Ocho, and the shooting and paralyzing of German Chub – abuses alleged to have been committed by mine company security personnel at HudBay’s former mining project in Guatemala. In a precedent-setting ruling with national and international implications, Superior Court of Ontario Justice Carole Brown has ruled that Canadian company Hudbay Minerals can potentially be held legally responsible in Canada for rapes and murder at a mining project formerly owned by Hudbay’s subsidiary in Guatemala. As a result of Justice Brown’s ruling, the claims of 13 Mayan Guatemalans will proceed to trial in Canadian courts. As a result of this ruling, Canadian mining corporations can no longer hide behind their legal corporate structure to abdicate responsibility for human rights abuses that take place at foreign mines under their control at various locations throughout the world. There will now be a trial regarding the abuses that were committed in Guatemala, and this trial will be in a courtroom in Canada, a few blocks from Hudbay’s headquarters, exactly where it belongs. Hudbay argued in court that corporate head offices could never be held responsible for harms at their subsidiaries, no matter how involved they were in on-the-ground operations. Justice Brown disagreed and concluded that “the actions as against Hudbay and HMI should not be dismissed.” This is the second significant legal victory for the Mayan plaintiffs in 2013. In February 2013, Hudbay abruptly dropped its argument that the lawsuit against it should be heard in Guatemala.

20

Two judgments handed down in the last year have caused renewed interest in the court's ability to 'pierce the veil of incorporation'. The starkly contrasting decisions given by Mr Justice Burton in Antonio Gramsci Shipping Corp v Stepanovs [2011] EWHC 333 (Comm) ("Gramsci"), and by Mr Justice Arnold in VTB Capital plc v Nutritek International Corp [2011] EWHC 3107 (Ch) ("VTB Capital") have provoked debate about the scope of the concept. In VTB Capital, the plaintiffs sued originally in Tort (for deceit) and then in Contract. VTB declined to follow Gramsci, and the Courts found that they could not lift the Corporate veil. Proceedings should have taken place in Russia, where Torts were committed, and all of the evidence and testimony would be in Russian. What’s important to note, however, is that Burton’s judgement in Gramsci is overruled by VTB Capital. In VTB Capital Arnold concluded, quoting a age from Justice Mumby in Ben Hashem v Ali Shayif, that the courts have only taken the step of piercing the corporate veil when 'the company was being used by its controller in an attempt to immunise himself from liability for some wrongdoing which existed entirely dehors the company'. He went on to explain that a wrongdoing 'dehors' the company is one which is 'anterior or independent' of it. This was the case in both Gilford and Jones; both Mr Horne and Mr Lipman attempted to avoid liability for their own wrongdoing by using a company that they controlled as a shield. In those circumstances the courts were willing to grant relief against their respective companies in order to prevent the claimants being denied an effective remedy. It is important to note that in both cases it was an equitable remedy, rather than damages, which the court awarded after piercing the corporate veil. In Gramsci the claimants successfully argued that the corporate veil should be pierced and Mr Stepanovs treated as a party to certain agreements entered into between the claimants and five companies ed in the British Virgin Islands and Gibraltar, one of which was beneficially owned by Mr Stepanovs. Mr Justice Burton held that there was a good arguable case that the claimants should be able to enforce a contract against Mr Stepanovs, the 'puppeteer', despite the contracts being entered into by his 'puppet' company. This was a potentially radical decision as it raised the prospect of non-parties being made liable on a contract to which it was not a signatory and at the same time raising the issue as to whether the 'puppeteer' was bound by all the of the contract. In reaching his conclusion Burton made a number of findings regarding the court's ability to pierce the corporate veil, which have subsequently received strong criticism from Mr Justice Arnold in VTB Capital. In VTB Capital, the claimants applied to amend their particulars of claim in order to bring a contractual claim against Mr Malofeev, Marcap BVI and Marcap Moscow, despite these defendants not being parties to the loan facility under which the claimants claimed to have been defrauded. Arnold J was therefore required to consider the law regarding piercing the corporate veil, and in declining to follow Gramsci took the opportunity to criticise the judgment given by Burton and to set out the circumstance he believed would justify the courts taking this step and the remedies available once the corporate veil is pierced. In Gramsci, Burton J held that the corporate veil could be pierced, and a claim for damages made, if the conditions in Trustor v Smallbone (No 2) [2001] WLR 1177 ("Trustor") were satisfied. These are (1) fraudulent misuse of the company structure, and (2) a wrongdoing committed 'dehors' the company.12 Arnold J rejected this finding, stating in particular that he did not agree that there can be a claim for common law damages, as distinct from an equitable remedy, whenever the Trustor conditions are satisfied. Arnold J went on to say that a number of authorities show that it is 'inappropriate', where a claim of wrongdoing is made against the controller of a company, to pierce the corporate veil to enable 21

a contractual claim against that person. In Arnold J's eyes, Trustor is instead authority for the proposition that, in a claim for knowing receipt, the court will treat receipt by a company as receipt by the individual who controls it if both conditions above are satisfied. Finally, Arnold J was dissatisfied with Burton J's acceptance of the submission that the notional puppeteer can be made liable for a contract, but that "as a matter of public policy" he cannot enforce it. Arnold J asked why such a defendant, who is being treated by the courts as a party to a contract, should not be able to enforce rights within it such as a set off or cross claim for unpaid sums.

Macaura v Northern Assurance Co Ltd [1925] AC 619 *A company’s property is the property of the company as a separate person not the . Facts: Owner of Timber estate sold all the timber property to a company in which he owned almost all the shares. He was also the largest creditor. He insured the timber against fire by policies taken out in his own name. Timber was destroyed and he sued the insurance company. The HoL held that in order to have an insurable interest in property a person must have a legal or equitable interest in the property not merely a moral certainty of profiting or losing from the property. Lord Wrenbury: “My Lords, this appeal may be disposed of by saying that the corporator even if he holds all the share in the corporation, and that neither he nor any creditor of the company has any property legal or equitable in the assets of the corporation.”

Lee v Lee’s Air Farming Ltd [1961] AC 12: [A company can employ one of its under a contract of service] A company employed Mr. Lee who owned 2,999 of 3000 shares, was its only director and have been appointed ‘governing director’ for life. He was killed in the course of his work for the company. The company’s insurers alleged that there was no contract of service so that no claim could be made. Lord Morris of Borth-y-Gest: In their lordships’ view it is a logical consequence of the decision in Salomon that one person may function in dual capacities. There is no reason, therefore, to deny the possibility of a contractual relationship being created as between the deceased and the company. The Privy Council also rejected the insurers’ arguments. Lord Morris said “there appears to be no greater difficulty in holding that a man acting in one capacity can give orders to himself in another capacity than there is in holding that a man acting in one capacity can make a contract with himself in another capacity”.

LIABILITY FOR FRAUDULENT TRADING: “A person who is found to have been knowingly party to the carrying on of a business of a company with intent to defraud its creditors, or creditors of any other person, or for any other person, of for any fraudulent

22

purpose, may be declared by the court to be liable to make such contributions (if any) to the company’s assets as the court thinks proper” (Insolvency Act 86 s.213)( pg. 690) “A person who was knowingly party to a company’s fraudulent trading may be may be made liable to contribute to its assets only when it is wound up, but such a person may at any time be prosecuted for the criminal offence of knowingly being a party to fraudulent trading (CA 2006, s. 993). Section 214 Insolvency Act – ‘Wrongful Trading’ – comes into operation ONLY if a company goes into liquidation at a time when its assets are insufficient for the payment of its debts and other liabilities and the expenses of winding up (s.214). In order to establish liability to elements must be proved (1) knowledge that insolvent liquidation was unavoidable (2) and failure to take every step to minimise potential loss to creditors.

COMPANIES ACT 2006 PART 29 FRAUDULENT TRADING 933 Offence of Fraudulent Trading (1)If any business of a company is carried on with intent to defraud creditors of the company or creditors of any other person, or for any fraudulent purpose, every person who is knowingly a party to the carrying on of the business in that manner commits an offence. (2)This applies whether or not the company has been, or is in the course of being, wound up. (3)A person guilty of an offence under this section is liable— (a)on conviction on indictment, to imprisonment for a term not exceeding ten years or a fine (or both); (b)on summary conviction— (i)in England and Wales, to imprisonment for a term not exceeding twelve months or a fine not exceeding the statutory maximum (or both); (ii)in Scotland or Northern Ireland, to imprisonment for a term not exceeding six months or a fine not exceeding the statutory maximum (or both). CHAPTER 2 MINIMUM SHARE CAPITAL REQUIREMENT FOR PUBLIC COMPANIES 767 Consequences of doing business etc without a trading certificate (1)If a company does business or exercises any borrowing powers in contravention of section 761, an offence is committed by— (a)the company, and (b)every officer of the company who is in default. (2)A person guilty of an offence under subsection (1) is liable— (a)on conviction on indictment, to a fine; (b)on summary conviction, to a fine not exceeding the statutory maximum. (3)A contravention of section 761 does not affect the validity of a transaction entered into by the company, but if a company— (a)enters into a transaction in contravention of that section, and 23

(b)fails to comply with its obligations in connection with the transaction within 21 days from being called on to do so, the directors of the company are tly and severally liable to indemnify any other party to the transaction in respect of any loss or damage suffered by him by reason of the company's failure to comply with its obligations.

Insolvency Act 1986 Penalisation of directors and officers 213 Fraudulent trading. (1)If in the course of the winding up of a company it appears that any business of the company has been carried on with intent to defraud creditors of the company or creditors of any other person, or for any fraudulent purpose, the following has effect. (2)The court, on the application of the liquidator may declare that any persons who were knowingly parties to the carrying on of the business in the manner above-mentioned are to be liable to make such contributions (if any) to the company’s assets as the court thinks proper. 214 Wrongful trading. (1)Subject to subsection (3) below, if in the course of the winding up of a company it appears that subsection (2) of this section applies in relation to a person who is or has been a director of the company, the court, on the application of the liquidator, may declare that that person is to be liable to make such contribution (if any) to the company’s assets as the court thinks proper. (2)This subsection applies in relation to a person if— (a)the company has gone into insolvent liquidation, (b)at some time before the commencement of the winding up of the company, that person knew or ought to have concluded that there was no reasonable prospect that the company would avoid going into insolvent liquidation, and (c)that person was a director of the company at that time; but the court shall not make a declaration under this section in any case where the time mentioned in paragraph (b) above was before 28th April 1986. (3)The court shall not make a declaration under this section with respect to any person if it is satisfied that after the condition specified in subsection (2)(b) was first satisfied in relation to him that person took every step with a view to minimising the potential loss to the company’s creditors as (assuming him to have known that there was no reasonable prospect that the company would avoid going into insolvent liquidation) he ought to have taken. (4)For the purposes of subsections (2) and (3), the facts which a director of a company ought to know or ascertain, the conclusions which he ought to reach and the steps which he ought to take are those which would be known or ascertained, or reached or taken, by a reasonably diligent person having both— (a)the general knowledge, skill and experience that may reasonably be expected of a person carrying out the same functions as are carried out by that director in relation to the company, and (b)the general knowledge, skill and experience that that director has. (5)The reference in subsection (4) to the functions carried out in relation to a company by a director of the company includes any functions which he does not carry out but which have been entrusted to him. (6)For the purposes of this section a company goes into insolvent liquidation if it goes into liquidation at a time when its assets are insufficient for the payment of its debts and other liabilities and the expenses of the winding up. 24